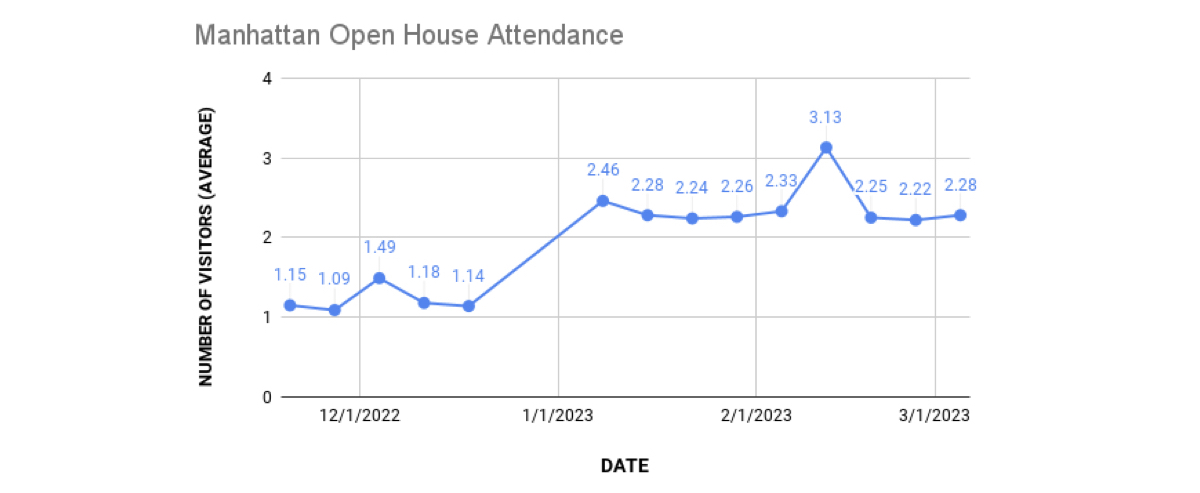

The February data in Manhattan seems counterintuitive at first given that the prevailing sentiment we hear is that there is "no inventory." Inventory is in fact not off from historical trends -- overall supply is close to normal levels and new listings coming on the market are over 400/week which is expected for late February. Buyer interest has also picked up substantially based on open house attendance and anecdotally on the response we've been getting on our listings. So why are signed contracts still down substantially year-over-year and compared to historical averages? The answer seems to be the unusually high number of listings being taken off the market by sellers. Listings being taken off market are up drastically year-over-year (10% marketwide and over 25% for resale) and even more compared to an average year (e.g. number of resale listings taken off-market is 33% higher than February 2019). Sellers who are not getting the offers they want are more readily pulling off-market to either wait it out or rent out the properties rather than adjusting pricing or expectations to make deals happen. New listings are being absorbed quickly, leading many buyers to feel like existing inventory has grown stale. With buyers interested but in no hurry to transact, they simply seem to be waiting for more options. Without a glut of new listings or adjusted seller behavior, we are unlikely to see contract figures catch up to historical levels this Spring. It is important to note that despite being below historical figures, the market is much stronger than the Fall. February closed with five straight weeks of growth in the number of signed contracts (with a blip during President's Day week) and the end of the month seemed to be trending upward closer to historical levels. Buyer activity at Manhattan open houses has remained consistent since the start of the year – 2.2-3.1 visitors per open house on average, which is higher than anything we saw in Q4 of 2022. |

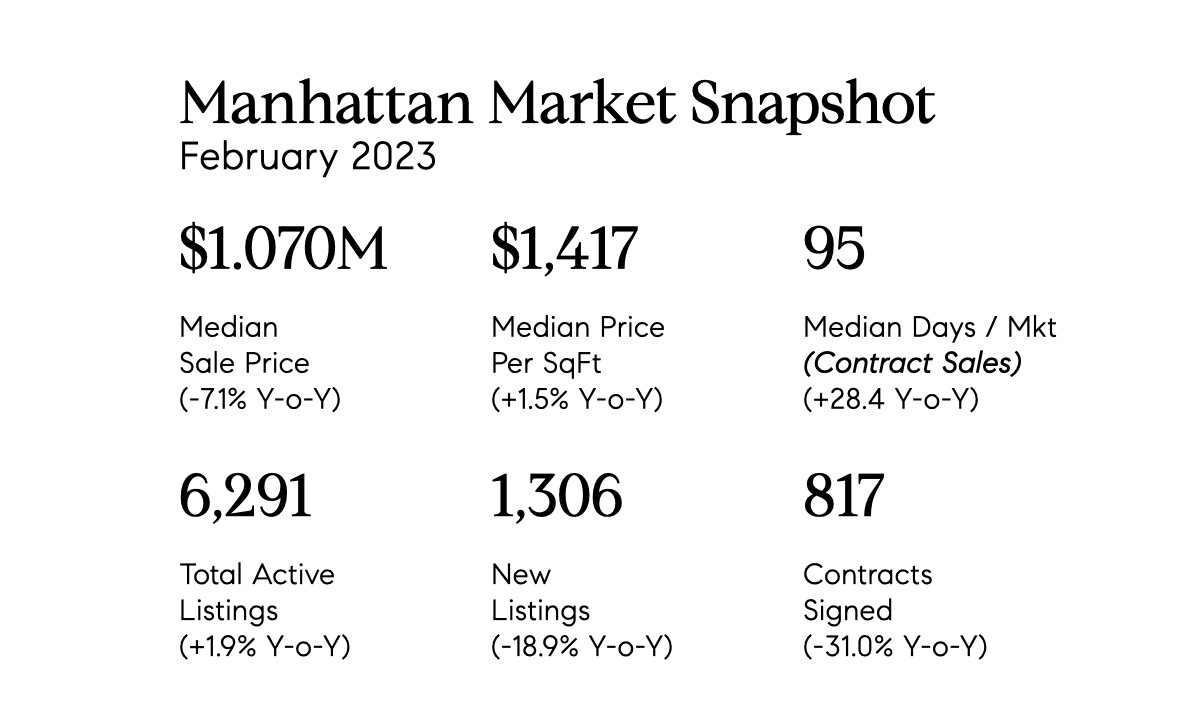

Manhattan median closed sale prices during February declined about ~7% year-over-year, but we expected this since these deals were negotiated in Q4 of 2022, what many consider the bottom of the market. On the ground now, prices for new listings do not seem to reflect further discounts. Median PPSF -- which is a measure of condo, not coop, pricing -- ticked up slightly in February hitting record levels according some data sources. Rather than indicate an upward shift in prices, our best guess to explain this trend is that only the strongest (more luxurious or in better condition) condos entered the market in the second half of the year, with sellers of weaker units sitting tight until the overall market improved. |

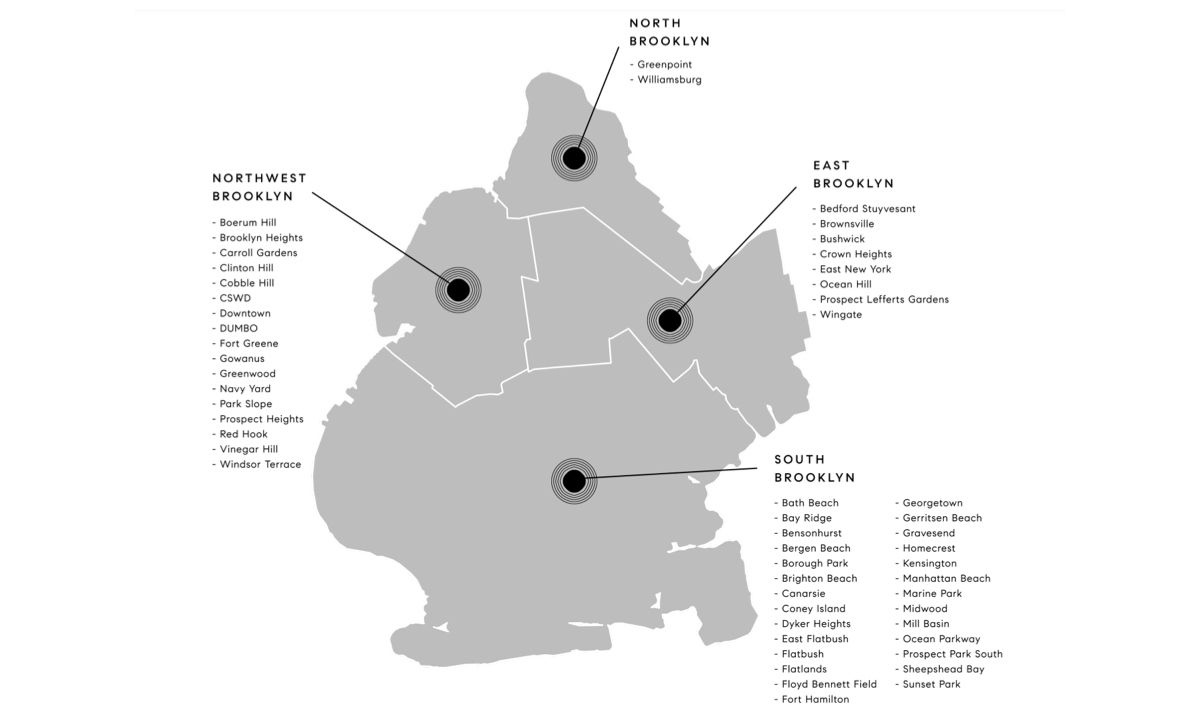

In Brooklyn, some have pronounced that the borough is entering a "buyer's market" but this does not reflect what many of our buyers continue to experience. This is because Brooklyn is the proverbial tale of two cities. Some areas of Brooklyn have declined (with overall supply up and lower demand) creating pockets of opportunity for buyers and bringing down overall metrics. However, competition remains fierce in other areas of the borough (i.e. NW Brooklyn, which includes areas like BK Heights, Fort Greene, DUMBO, Park Slope, BOCOCA and Prospect Heights), where demand continues to dramatically out-pace supply. |

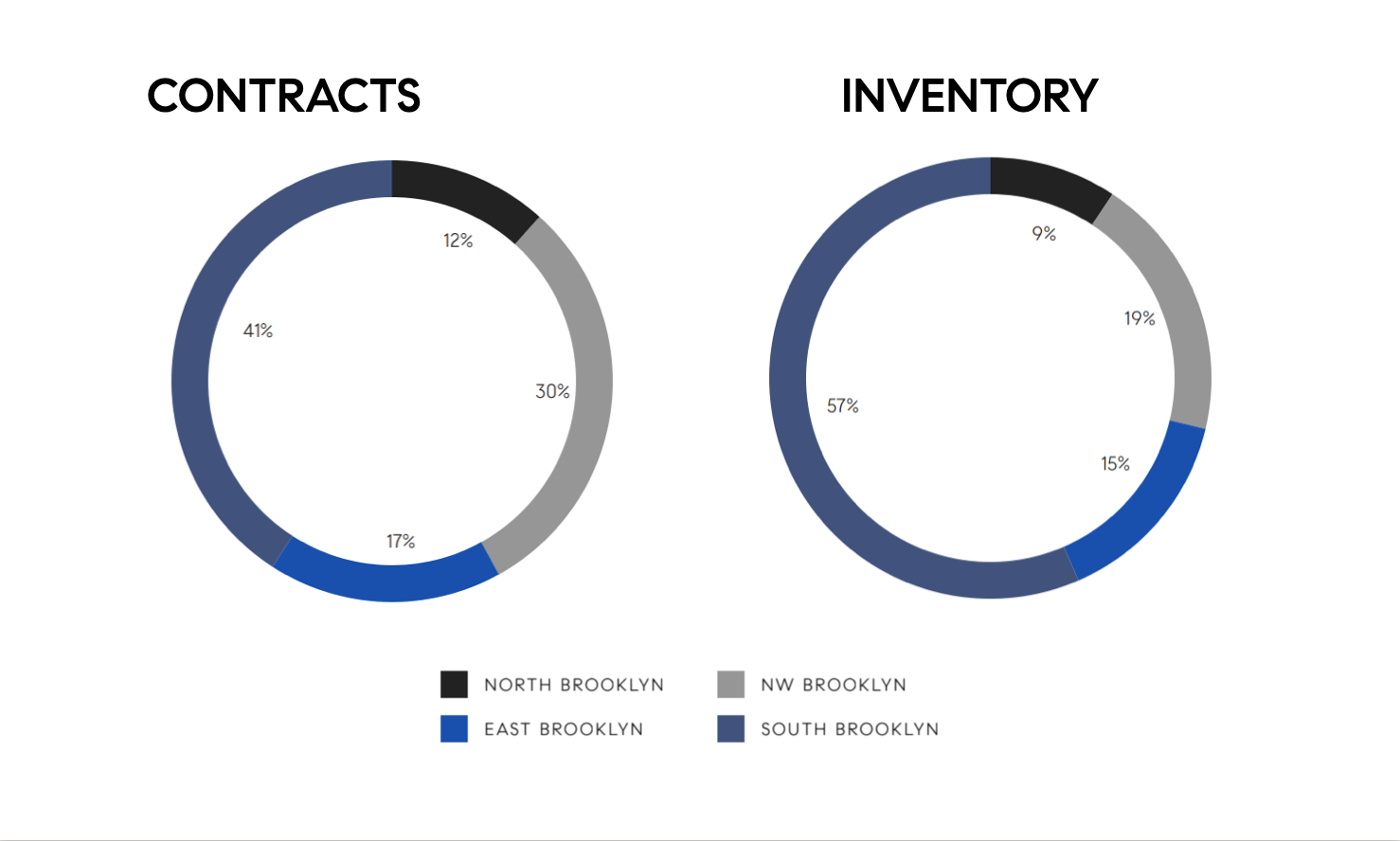

In February, South Brooklyn (everything south of the Prospect Expressway) accounted for 57% of total inventory but only 41% of contracts. On the flip side, listings in NW and North Brooklyn (Greenpoint & Williamsburg) made up 28% of total inventory but a whopping 42% of February contracts. While there is some variation between inventory / contract activity in certain areas of Manhattan, it is nowhere near this magnitude. The disparity has made marketwide Brooklyn figures (and headlines) somewhat meaningless, and it is critical to have an advisor familiar with the sub-markets to be able to provide accurate advice. |

While it remains to be seen how 2023 will unfold, anecdotally we've recently had good traffic at all our new Manhattan listings, while our Brooklyn buyers have been frustrated by very minimal new inventory. Assuming interest rates remain stable, we are cautiously optimistic for the year but expect transaction levels to remain below historical averages at least through the Spring market unless there is a shift in seller sentiment. |

After months of going down, mortgage rates have risen again, now up 0.75% from where they were at the start of February. |

While some BK metrics suggest an increasing buyer's market, but on the ground buyer demand has remained strong and discounts remain hard to find. ( FORBES) |

A new study by RentCase highlights some interesting data points, notably that three NYC boroughs are home to some of the smallest apartments in the county... other top-5-smallest locales include Seattle & Portland. |

Ranking NYC's Most Expensive Neighborhoods - Nolita officially unseated Billionaires’ Row for the highest average price in 2022 ( TRD) |

Want to indulge in some real estate fantasies and see how the ultra rich live? Check out Compass's Ultra Luxury Report. |

With all the noise about the housing market nationally and locally, it is important to note that real estate -- especially in NYC -- is hyper local. Every neighborhood, block, even building, is impacted differently by macroeconomic conditions, and the market can differ wildly for specific price points or property types. While we hope you find these reports helpful in discerning trends in NYC, they may not reflect how your property might perform or what to expect from your home search. If you have questions, we are always here to provide a consultation.

|

Make sure to take a peek at our current and upcoming listings below. We’ll be back next month with more real estate news. Until next time! |

|

© Compass 2023 ¦ All Rights Reserved by Compass ¦ Made in NYC

Compass is a licensed real estate broker. All material is intended for informational

purposes only and is compiled from sources deemed reliable but is subject to

errors, omissions, changes in price, condition, sale, or withdrawal without

notice. No statement is made as to the accuracy of any description or measurements

(including square footage). This is not intended to solicit property already listed.

No financial or legal advice provided. Equal Housing Opportunity.

All Coming Soon listings in NYC are simultaneously syndicated to the REBNY RLS.

Photos may be virtually staged or digitally enhanced and may not reflect

actual property conditions.

marketingcenter-newyorkcity-manhattan

|

|

|