|

|

|

|

Temperatures are high as we enter Q3 2024, but what about the temperature of the NYC real estate market? In this month's newsletter, we delve into the Q2 2024 update, discuss the latest real estate news, and more. |

|

|

|

|

|

|

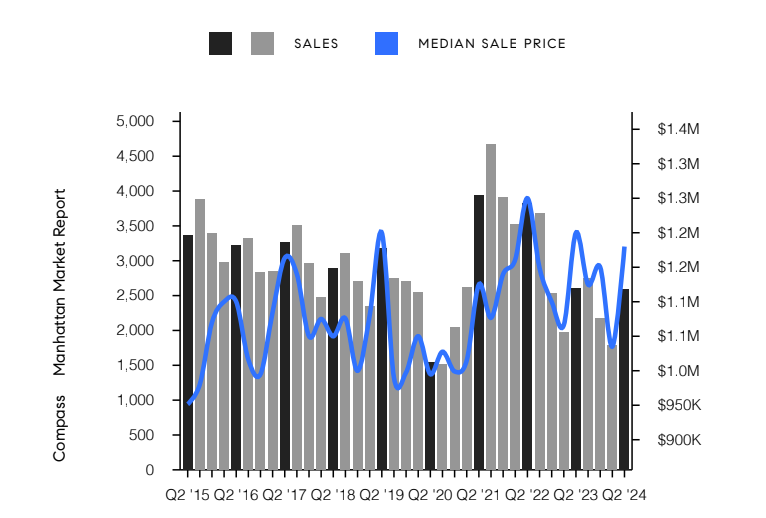

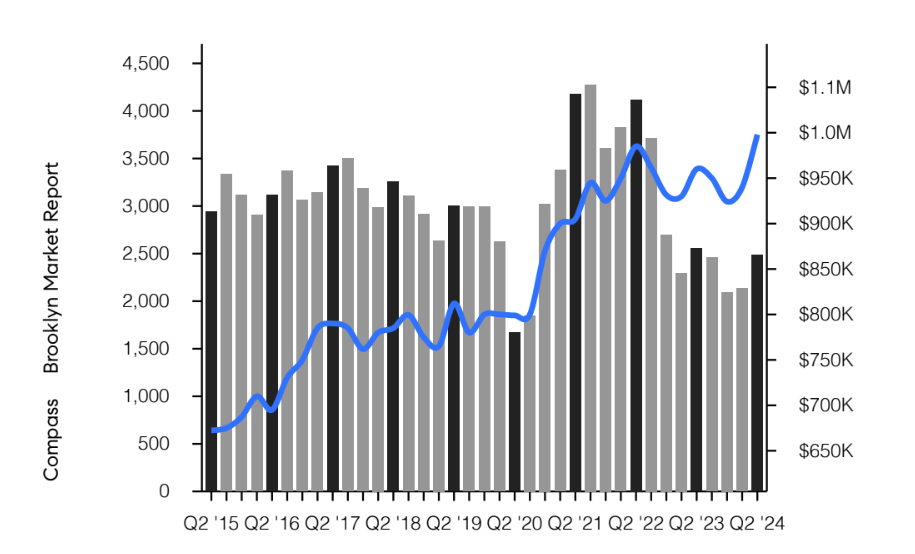

| | Manhattan is shifting towards a buyer’s market as apartment prices dropped and inventory rose in the second quarter of 2024, according to recent reports. The average sales price for real estate in Manhattan declined by 3%, bringing it to just over $2M. The median price experienced an almost 2% decrease YOY, settling at $1.2M, with luxury apartment prices falling for the first time in more than a year. These price drops are due to an increasing number of apartments available for sale, which are also remaining on the market for longer periods. Currently, more than 8,000 apartments are listed in Manhattan, exceeding the 10-year average of around 7,000, according to Jonathan Miller, CEO of Miller Samuel, a firm specializing in appraisal and research. Manhattan now has a 9.8-month supply of apartments, meaning it would take nearly 10 months to sell all the available units without new listings. Generally, a supply exceeding six months is considered indicative of a buyer’s market. Experts indicate that the trend of declining prices and increasing inventory in Manhattan is due to the unsustainability of the previously strong post-Covid prices. This shift has prompted both buyers and sellers to adapt to the current higher interest rate environment. As the disparity between buyer and seller expectations narrows, more transactions are being completed. There were 2,609 sales in the second quarter, a 12% increase from the previous year, marking the first sales increase in two years. High rental prices in Manhattan are also contributing to increased sales. In May, the average rental price remained above $5,100 per month. Many potential buyers who had been renting are now choosing to purchase, hoping that interest rates will decrease by late 2024 or early 2025. Current mortgage rates are seemingly having a lesser impact on the sales market than previously observed. Annually, cash deals rose by 10.6%, while mortgage-related transactions saw an increase of more than 15%. Despite this shift, cash deals still accounted for 62.3% of all transactions. Although prices fell across all segments of the Manhattan real estate market, the luxury segment is particularly weak. Wealthy buyers are postponing purchases due to uncertainties surrounding the upcoming elections. The median sale price for luxury properties, representing the top 10% of the market, dropped by 11% in the second quarter, and inventory increased by 22.4%. The observed weakness in the luxury market may indicate a developing trend or could simply be a temporary fluctuation, with more clarity expected in the second half of the year. In Brooklyn, listing inventory increased for the first time in nine quarters, with a 14.5% increase compared to the previous year, indicating 4.4 months of supply versus 3.5 months in 2023. Despite increased inventory, median prices across all property types, including condos, co-ops, and houses, increased by 4.2% for both the quarter and the year. The average price per square foot for co-op sales, however, dropped 6% to $570. By the same metric, condo prices rose 3% for the year to $1,029 for resales and $1,437 for new developments. In Northwest Brooklyn's brownstone market, which includes one to three-family homes, the price per square foot soared by 45.3% YOY, as reported by Miller Samuel. This quarter saw 84 sales, with the average price per square foot reaching $2,033—a 1.6% rise from the first quarter's $2,001 per square foot and a significant increase from $1,399 a year earlier. Brooklyn’s real estate market in Q2 of 2024 exhibited a mix of indicators, yet the overall trend leaned positively, suggesting a recovering market. The increase in prices and listings underscores Brooklyn’s appeal and competitive edge. Let's take a closer look at sales trends in Manhattan and Brooklyn. |

|

|

|

|

|

|

|

| | | | | | Properties That Spent 180+ DOM |

|

|

|

|

| | | | Source: Compass Q2 2024 Manhattan Market Report |

|

|

|

|

| | | | | | Contracts Signed Year-Over-Year |

|

|

|

|

| | | | Properties That Spent 180+ DOM |

|

|

|

|

| | | | Source: Compass Q2 2024 Brooklyn Market Report |

|

|

|

|

|

|

| | | The Rent Guidelines Board voted on June 17th to allow landlords to raise rents on rent stabilized apartments. The official numbers are +2.75% for one-year leases and +5.25% for two-year leases, effective October 1, 2024. This is the third year in a row the Adams-appointed board has voted (narrowly) in favor of an increase. According to data provided by Miller Samuel, 24% of landlords of market value units rented their properties for more than their initial asking price. Overall, the June rental market trends are much the same as they have been, with record high rents holding relatively steady. The shift, though, is that with those same record rents, the square footage is dropping. Renters, especially in Manhattan, are paying the same amount for less space. |

|

|

|

|

| |

|

| With the 2024 presidential election approaching, the pressing question for buyers, sellers, and investors is how the election will shape real estate markets. The market is fundamentally driven by supply and demand, which is affected by various factors including economic conditions, government policies, demographics, interest rates, available capital, and location. The influence of elections on these factors is more nuanced and abstract, often compared to singular events like natural disasters, which can cause uncertainty but usually have a localized impact. Historically, presidential elections have only had a minimal, short-term effect on the housing market. In presidential election years, November usually sees a slight dip in home sales. This hesitation stems from uncertainty surrounding the election. However, this slowdown is temporary. Data from the Department of Housing and Urban Development (HUD) and the National Association of Realtors (NAR) shows that after nine of the last 11 presidential elections, home sales increased the following year (see graph below). |

| | Contrary to some concerns, home prices typically do not drop during election years. Home prices tend to rise year-over-year, irrespective of elections. According to NAR data, after seven of the last eight presidential elections, home prices increased the subsequent year (see graph below). |

| | The only exception was during the housing market crash, which was an anomaly compared to typical market conditions. Today's market is more stable, and historical trends suggest that home values are likely to continue rising after elections. Similarly, mortgage rates, a critical factor in home affordability, are more influenced by broader economic conditions than by national elections. Over the past few years, mortgage rates have been highly volatile, driven by factors beyond the control of any election or administration. While national elections can influence economic policies and consumer confidence, their direct impact on mortgage rates is limited. Analyzing the last 11 presidential election years, Freddie Mac data shows that mortgage rates decreased from July to November in eight of those years (see chart below). |

| | Most forecasts suggest that mortgage rates may ease slightly toward the end of this year. If these predictions hold, it will result in lower monthly payments for homebuyers. While presidential elections do have some impact on the housing market, these effects are generally small and short-lived. Local elections, such as those for New York Governor and NYC Mayor, often impact the real estate market more than national ones. These elections can change land use policies and zoning regulations, affecting housing availability and affordability, which can create uncertainty and cause delays in buying and selling decisions. Understanding these dynamics can help buyers and sellers navigate the market more effectively during an election year. |

| |

|

|

|

|

|

|

| This year's annual cyclist and pedestrian paradise is set to be the biggest one ever. The DOT has announced that it will be extending the hours of the beloved initiative to allow more New Yorkers to take advantage of the miles of streets that will be closed to car trafficacross all five boroughs. This is the first extension of Summer Streets' hours since 2008. Now, instead of ending at 1 PM, the program will run from 7 AM to 3 PM. According to the DOT, more than half a million people come out to enjoy the extra walkable space and special activities along the closed routes. The closures will be happening throughout the city over the course of four Saturdays, starting July 27th and going until August 24th. Click here for more information. |

|

|

|

|

|

|

|

|

| 88 Lexington Avenue, Unit 1003 |

| 2 BD 2.5 BA 1,541 SF $12,500/month |

| This luxurious east-facing split two-bedroom, two-and-a-half-bathroom home features oversized windows with open views, ceilings over 10 feet high, an in-unit washer/dryer, a separate office area, and central AC, all a building with more than 10,000 square feet of amenities. |

|

|

| | |

|

|

|

| | | 265 East Houston Street, Unit 7 |

| 2 BD 2 BA 1,400 SF $9,995/month |

| Available short term (three months minimum) or long term, furnished, unfurnished, or partially furnished.

Ideally located in the heart of the Lower East Side, this expansive seventh-floor loft-style home offers unparalleled luxury living. |

|

|

|

|

|

|

|

| | | 174 East 74th Street, Unit 10G |

| 2 BD 1 BA 850 SF $799,000 |

| With approximately 850 square feet of living space, this inviting home boasts east-facing windows that bathe the interior in sunshine throughout the day, offers abundant closet space, the ability to install a washer/dryer, and an incredibly low-maintenance, all in a full-service coop ideally positioned west of Third Avenue. |

|

|

|

|

|

|

|

| 645 East 11th Street, Unit 1F |

| | Located in the East Village, this retail condo was formerly a dental office. There are three exam rooms and two street entrances. |

|

|

| | |

|

|

|

|

| | 20 Pine Street, Unit 2002 |

| |

|

|

| | | | 60 East 12th Street, Unit 5K |

| |

|

|

|

|

|

|

| | | 251 East 32nd Street, Unit 5J |

| 1 BD 1 BA 775 SF $599,000 |

| This recently renovated home is sunny, spacious, remarkably quiet, and boasts ample closet and storage space. Featuring wide-plank white oak floors and charming views of townhouse gardens through expansive windows, the apartment exudes a bright and cheerful atmosphere. |

|

|

|

|

|

|

| 376 President Street, Unit 1B |

| 2 BD 3 BA 1,367 SF $1,565,000 |

| Discover the late Victorian industrial charm of Carroll Gardens in this highly unique two-bedroom, three-bath condo at the iconic Mill Building. Brimming with vintage factory details, this expansive sunlit unit boasts an open Northern exposure and the kind of inviting warmth and soul you simply can’t find in a new build. |

|

|

| | |

|

|

|

| | | | 1 BD 1 BA 750 SF $599,000 |

| This sunny, spacious, renovated home has open city views from southern and western exposures. The apartment features hardwood floors, an open kitchen with stainless steel appliances, and six large closets, including two California closets. |

|

|

|

|

|

|

|

| Perfect for an investor or end user. Tenant in place paying $7,750/month. Contact me for details. Perched on the 30th floor with breathtaking views from three different exposures, this expansive home has been fully renovated, and not a single detail has been overlooked. Enjoy 75 square feet of private outdoor space, an open chef’s kitchen with top-of-the-line appliances and a large island, and laundry just down the hall, all in a full-service condo. |

|

|

| | |

|

|

|

|

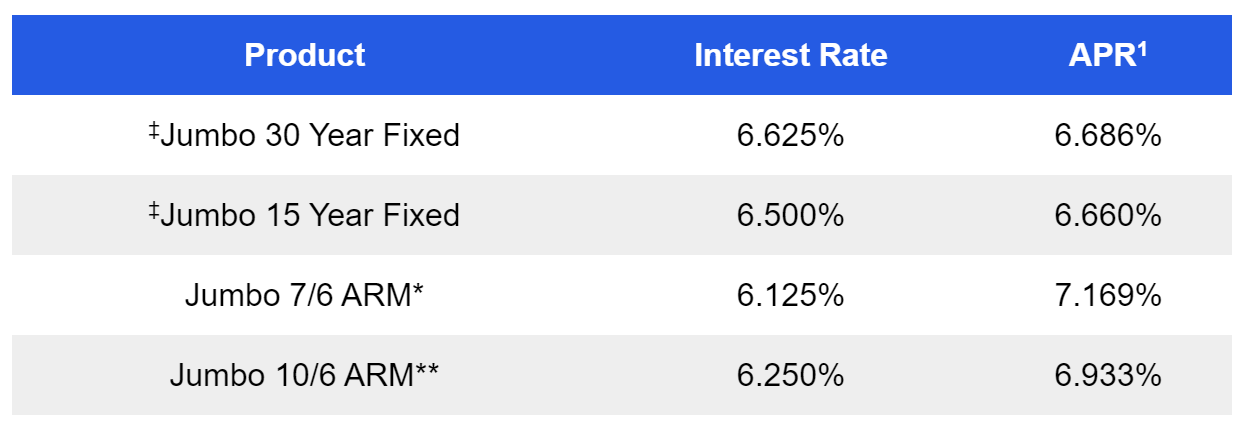

Most Recent Mortgage Rates |

| | Rates are from Citibank and are effective as of 07/12/2024. Rates are subject to change without notice. |

| Everyone’s mortgage needs are different. I have great relationships with mortgage brokers and loan officers from big banks and small banks who can help find the best loan for you. If you're looking for a lender you can trust, I'd love to help. Email me for more. |

| | | I'm an expert at successfully repositioning and selling homes that were previously listed without success. Click here for examples of how I have transformed listings to showcase a property's full potential, securing favorable deals where other agents could not. |

| Find out how Compass Concierge can help you prepare your home before coming to market by fronting the costs of upgrading, renovating, and staging at no interest. |

| I'm born and raised in New York City. If you've got a question, I've got you covered. For recommendations on anything, from how to find day passes for the hottest hotels with rooftop pools to which co-ops have the best amenities, it's as simple as sending me an email. |

|

|

|

|

|

|

| | Licensed Associate Real Estate Broker |

|

|

| | |

|

|

|

|

Office: 646-982-0353 Compass is a licensed real estate broker. All material is intended for informational purposes only and is compiled from sources deemed reliable but is subject to errors, omissions, changes in price, condition, sale, or withdrawal without notice. No statement is made as to the accuracy of any description or measurements (including square footage). This is not intended to solicit property already listed. No financial or legal advice provided. Equal Housing Opportunity. All Coming Soon listings in NYC are simultaneously syndicated to the REBNY RLS. Photos may be virtually staged or digitally enhanced and may not reflect actual property conditions. |

|

|

|

|

|

|